5

MIN READ

What is an IBAN and what is it used for?

Table of contents

IBAN stands for International Bank Account Number, the international bank account number.

It's a combination of letters and numbers that uniquely identifies a bank account in any country that uses this format.

Before the IBAN existed, each country had its own account format, and sending a transfer to another European country was a slow process with plenty of room for error, because banks in different countries didn't "speak the same language" when it came to identifying accounts. In 1997, the European Committee for Banking Standards (ECBS) standardized the system under the ISO standard to address that problem.

In Spain, the transition was finalized on February 1, 2014, the date from which the old 20-digit Código de Cuenta Cliente (CCC) was no longer accepted as a valid format and was absorbed into the 24-character IBAN.

How the IBAN is structured

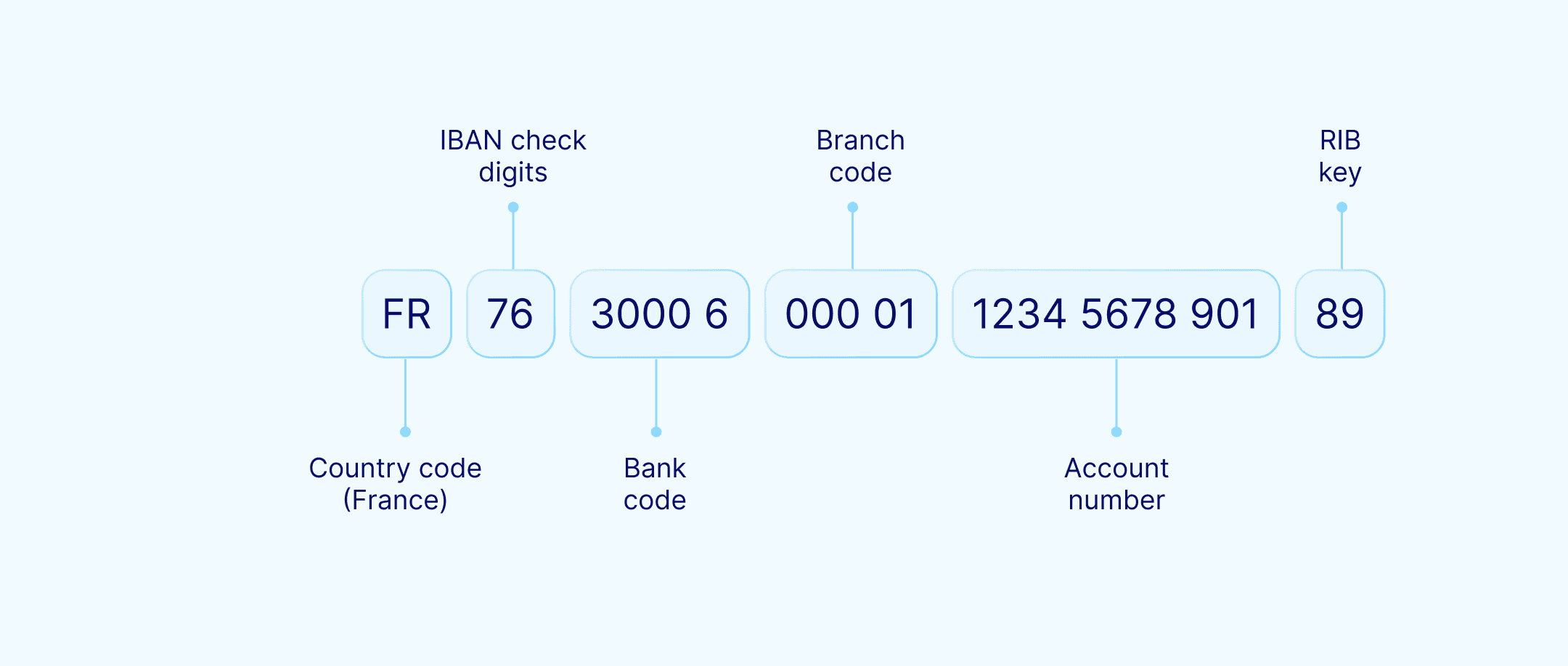

The number of characters in an IBAN varies by country. In Spain, it always has 24 characters.

The first 4 characters identify the country and serve as an error check:

2 letters → country code (ES for Spain)

2 digits → IBAN check digits

The remaining 20 characters are the bank account number, broken down as follows:

4 digits → bank code

4 digits → branch code

2 digits → account check digits

10 digits → customer account number

For example:

The length of the IBAN varies by country. In Germany it has 22 characters, and in France 27. Even though the formats differ, all are internationally valid within the IBAN standard, which today is used in more than 85 countries, including Turkey, Brazil, and the United Arab Emirates.

It's worth noting that countries not covered by the IBAN standard have their own systems for identifying accounts.

The United States, for example, uses two separate codes:

ABA Routing Number (9 digits): identifies the bank, equivalent to a BIC but for domestic transactions.

Account Number (7–12 digits): identifies the specific account.

What the IBAN is used for

Its primary function is to identify the destination account in a bank transfer. But it's also used for other operations, such as:

Setting up direct debits: in Spain, when you authorize a company to charge your account for a gas bill, a gym membership, or a phone invoice, what you give them is your IBAN.

Receiving your salary: your employer needs your IBAN to deposit your pay each month.

Managing Social Security contributions: self-employed workers also need their IBAN to set up their monthly payments.

IBAN, BIC, and SWIFT: what's the difference?

As we've seen, the IBAN is the number that identifies a bank account and is used in countries like Spain.

BIC and SWIFT, on the other hand (they actually refer to the same code), are used to locate the bank (and even the branch) where the account is held.

SWIFT (Society for Worldwide Interbank Financial Telecommunication) is the organization that manages the network connecting more than 9,000 financial institutions worldwide.

BIC (Business Identifier Code, though it's also commonly referred to as Bank Identifier Code) is the technical name of the code used by the SWIFT network.

Your bank provides the BIC/SWIFT code directly, and you can find it in:

Your bank's app or website, in the account details section

Any bank statement

The BIC/SWIFT code is between 8 and 11 characters long:

4 alphanumeric characters → institution prefix

2 alphabetic characters → country code per ISO 3166-1 (the international standard - that defines two-letter country codes)

2 alphanumeric characters → institution suffix

3 optional characters → branch code

For example, the BIC code for BBVA in Madrid, Spain is BBVAESMM

BBVA → BBVA institution

ES → Spain's country code

MM → location code, in this case Madrid

With the branch code added, the total comes to 11 characters.

When your bank initiates an international transfer outside the SEPA zone, it generates an encrypted message containing all the details of the transaction, including the date, currencies, amount, and so on. That message travels through the SWIFT network, and the BIC/SWIFT code is what identifies the receiving bank.

What happens if you enter the wrong IBAN

If you make a mistake when entering an IBAN for a transfer, one of two things can happen:

The IBAN doesn't exist at any bank, in which case the transfer doesn't go through. The system catches this thanks to the check digits and returns the funds.

The IBAN does belong to a real account. In that case, the money reaches that account. Under Spanish law (Royal Decree-Law 19/2018, Article 59, transposing the European Payment Services Directive) the bank is only obligated to execute the transfer based on the IBAN. If the code was technically valid, even if it was wrong, the bank bears no responsibility for the error.

What your bank is required to do is attempt to recover the funds, which requires the cooperation of the receiving bank. That process has no guaranteed timeline or assured outcome. If the account holder who received the money by mistake doesn't return it voluntarily, the only remaining option is legal action.

There's a relevant regulatory change: since October 9, 2025, Regulation (EU) 2024/886 requires payment service providers to verify that the beneficiary's name matches the IBAN before executing euro transfers within the SEPA zone. If there's a discrepancy, the bank must alert the customer before processing the transaction.

For all these reasons, it's worth checking the IBAN character by character before confirming any transaction, especially if it's the first time you're sending money to that account.

How to find your IBAN

The easiest way is to check your bank's app. Go to the section with your account information and you'll find it there, along with the BIC/SWIFT code.

You can also find it in:

Your bank's website, in the customer area

Any bank statement

Any direct debit mandates you've signed

If you have your old account number in CCC format (the 20 digits without the ES prefix), you can convert it to an IBAN using an online calculator.

At Zru we help businesses manage their online payments from a single platform, connecting with more than 200 payment methods and processors, tailored to each business's needs. If you'd like to talk to our team, you can reach us here.

The content of this publication is provided for general informational and educational purposes only and does not constitute legal, tax, or professional advice of any kind. No guarantee is made that the information is accurate, complete, up to date, or suitable for specific situations. For advice tailored to your particular circumstances, you should consult a qualified attorney or tax advisor duly licensed in the relevant jurisdiction.

5

MIN READ

What is an IBAN and what is it used for?

Table of contents

IBAN stands for International Bank Account Number, the international bank account number.

It's a combination of letters and numbers that uniquely identifies a bank account in any country that uses this format.

Before the IBAN existed, each country had its own account format, and sending a transfer to another European country was a slow process with plenty of room for error, because banks in different countries didn't "speak the same language" when it came to identifying accounts. In 1997, the European Committee for Banking Standards (ECBS) standardized the system under the ISO standard to address that problem.

In Spain, the transition was finalized on February 1, 2014, the date from which the old 20-digit Código de Cuenta Cliente (CCC) was no longer accepted as a valid format and was absorbed into the 24-character IBAN.

How the IBAN is structured

The number of characters in an IBAN varies by country. In Spain, it always has 24 characters.

The first 4 characters identify the country and serve as an error check:

2 letters → country code (ES for Spain)

2 digits → IBAN check digits

The remaining 20 characters are the bank account number, broken down as follows:

4 digits → bank code

4 digits → branch code

2 digits → account check digits

10 digits → customer account number

For example:

The length of the IBAN varies by country. In Germany it has 22 characters, and in France 27. Even though the formats differ, all are internationally valid within the IBAN standard, which today is used in more than 85 countries, including Turkey, Brazil, and the United Arab Emirates.

It's worth noting that countries not covered by the IBAN standard have their own systems for identifying accounts.

The United States, for example, uses two separate codes:

ABA Routing Number (9 digits): identifies the bank, equivalent to a BIC but for domestic transactions.

Account Number (7–12 digits): identifies the specific account.

What the IBAN is used for

Its primary function is to identify the destination account in a bank transfer. But it's also used for other operations, such as:

Setting up direct debits: in Spain, when you authorize a company to charge your account for a gas bill, a gym membership, or a phone invoice, what you give them is your IBAN.

Receiving your salary: your employer needs your IBAN to deposit your pay each month.

Managing Social Security contributions: self-employed workers also need their IBAN to set up their monthly payments.

IBAN, BIC, and SWIFT: what's the difference?

As we've seen, the IBAN is the number that identifies a bank account and is used in countries like Spain.

BIC and SWIFT, on the other hand (they actually refer to the same code), are used to locate the bank (and even the branch) where the account is held.

SWIFT (Society for Worldwide Interbank Financial Telecommunication) is the organization that manages the network connecting more than 9,000 financial institutions worldwide.

BIC (Business Identifier Code, though it's also commonly referred to as Bank Identifier Code) is the technical name of the code used by the SWIFT network.

Your bank provides the BIC/SWIFT code directly, and you can find it in:

Your bank's app or website, in the account details section

Any bank statement

The BIC/SWIFT code is between 8 and 11 characters long:

4 alphanumeric characters → institution prefix

2 alphabetic characters → country code per ISO 3166-1 (the international standard - that defines two-letter country codes)

2 alphanumeric characters → institution suffix

3 optional characters → branch code

For example, the BIC code for BBVA in Madrid, Spain is BBVAESMM

BBVA → BBVA institution

ES → Spain's country code

MM → location code, in this case Madrid

With the branch code added, the total comes to 11 characters.

When your bank initiates an international transfer outside the SEPA zone, it generates an encrypted message containing all the details of the transaction, including the date, currencies, amount, and so on. That message travels through the SWIFT network, and the BIC/SWIFT code is what identifies the receiving bank.

What happens if you enter the wrong IBAN

If you make a mistake when entering an IBAN for a transfer, one of two things can happen:

The IBAN doesn't exist at any bank, in which case the transfer doesn't go through. The system catches this thanks to the check digits and returns the funds.

The IBAN does belong to a real account. In that case, the money reaches that account. Under Spanish law (Royal Decree-Law 19/2018, Article 59, transposing the European Payment Services Directive) the bank is only obligated to execute the transfer based on the IBAN. If the code was technically valid, even if it was wrong, the bank bears no responsibility for the error.

What your bank is required to do is attempt to recover the funds, which requires the cooperation of the receiving bank. That process has no guaranteed timeline or assured outcome. If the account holder who received the money by mistake doesn't return it voluntarily, the only remaining option is legal action.

There's a relevant regulatory change: since October 9, 2025, Regulation (EU) 2024/886 requires payment service providers to verify that the beneficiary's name matches the IBAN before executing euro transfers within the SEPA zone. If there's a discrepancy, the bank must alert the customer before processing the transaction.

For all these reasons, it's worth checking the IBAN character by character before confirming any transaction, especially if it's the first time you're sending money to that account.

How to find your IBAN

The easiest way is to check your bank's app. Go to the section with your account information and you'll find it there, along with the BIC/SWIFT code.

You can also find it in:

Your bank's website, in the customer area

Any bank statement

Any direct debit mandates you've signed

If you have your old account number in CCC format (the 20 digits without the ES prefix), you can convert it to an IBAN using an online calculator.

At Zru we help businesses manage their online payments from a single platform, connecting with more than 200 payment methods and processors, tailored to each business's needs. If you'd like to talk to our team, you can reach us here.

The content of this publication is provided for general informational and educational purposes only and does not constitute legal, tax, or professional advice of any kind. No guarantee is made that the information is accurate, complete, up to date, or suitable for specific situations. For advice tailored to your particular circumstances, you should consult a qualified attorney or tax advisor duly licensed in the relevant jurisdiction.